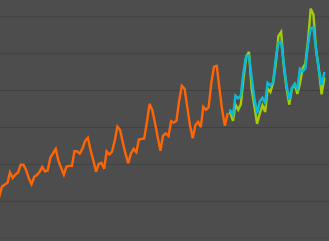

Expanded Time Series Processes

Mathematica Version 10 now includes fully automated fitting and diagnostics across the full suite of time series processes, making time series modeling an everyday exploratory tool. Time series modeling has also been deepened to include ARCH and GARCH processes, as well as vector-valued versions of standard time series models. The full time series model framework has been greatly enhanced, including simulation, estimation, and property computations.

|

|