Random Process Analysis

Enhanced Random Processes »

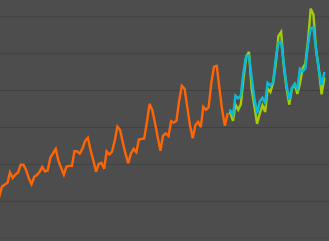

Mathematica Version 10 expands on the already extensive random process framework with new processes, including hidden Markov models. Hidden Markov models are typically used to infer the hidden internal state from emissions, as in communication decoding, speech recognition, and biological sequence analysis. The random process framework also adds advanced time series processes and transformations of existing processes, as well as significantly improves computation with slice distributions—the bridge from random processes to random variables - often giving definite conclusions about expected process behavior from models. |

|

Expanded Time Series Processes »

Mathematica Version 10 now includes fully automated fitting and diagnostics across the full suite of time series processes, making time series modeling an everyday exploratory tool. Time series modeling has also been deepened to include ARCH and GARCH processes, as well as vector-valued versions of standard time series models. The full time series model framework has been greatly enhanced, including simulation, estimation, and property computations. |

|