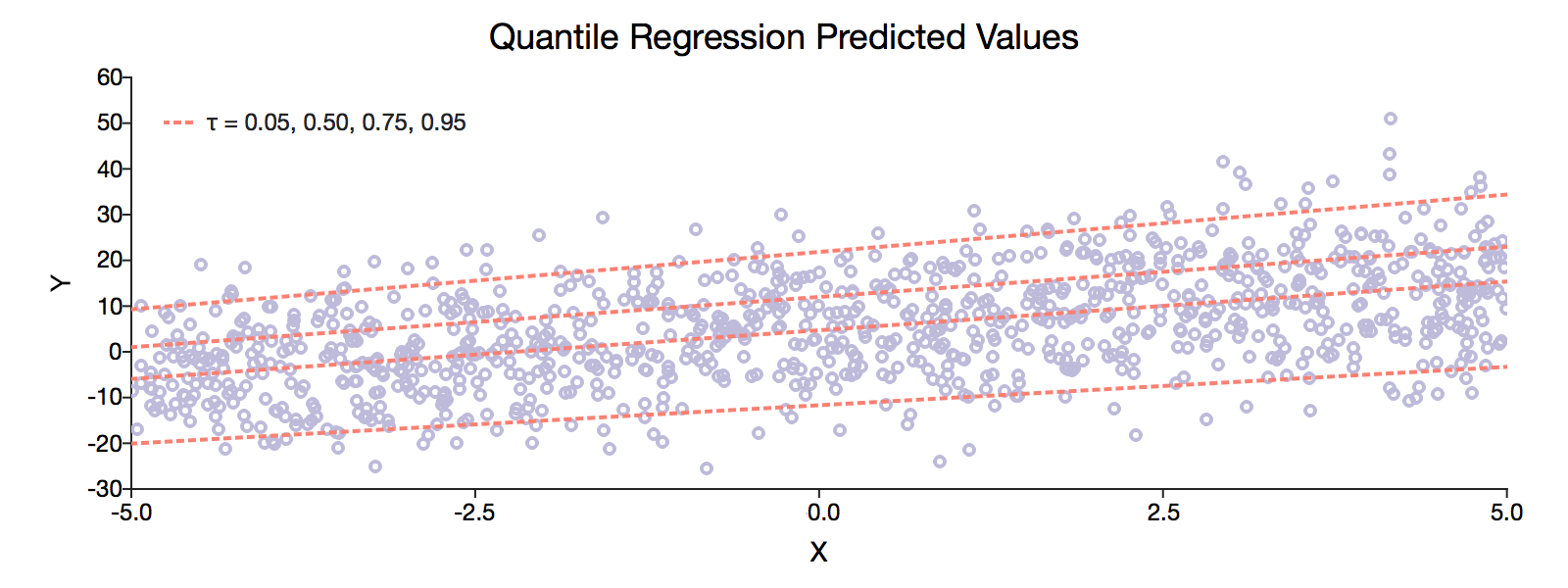

Quantile Regression in GAUSS 19

Choose from two quantile regression functions

- quantileFit provides parameter estimates and optional bootstrapped confidence intervals and standard errors for conditional quantile regressions.

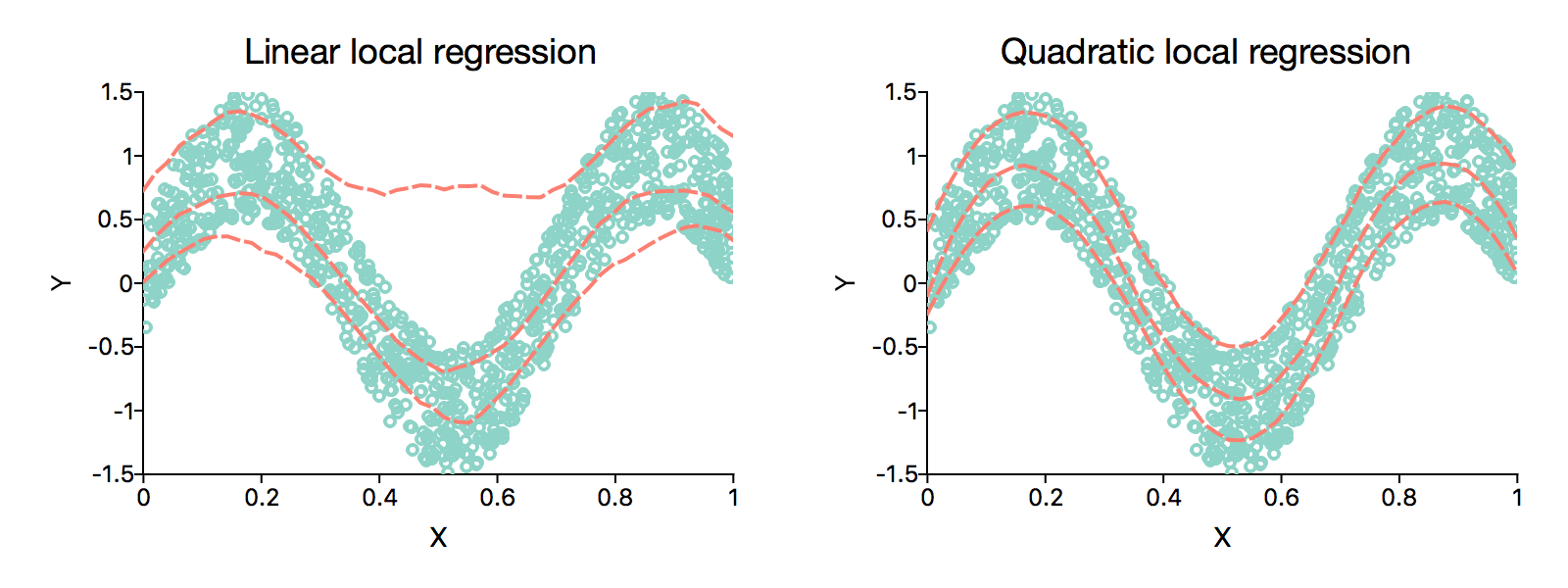

- quantileFitLoc estimates local linear and quadratic quantiles for specified quantile points.

Easy implementation

Both functions support formula strings and common default settings for quick estimation:

// Perform quantile regression estimation

call quantileFit(fname, "ln_wage ~ age + age:age + tenure");Custom options

- Bootstrapped parameter confidence intervals and standard errors.

- Interior point or quadratic programming algorithms.

- Iteration and results printing.

- User specified variable names for results printing.